Search posts

Don’t bank on rate cuts

Don’t bank on rate cuts

We expect the US will enter recession at some stage around the end of 2020. Oreana’s 2019 Medium-Term Global Outlook explains our concerns in detail. In summary, we think increasing leverage, rising rates, slowing growth and heightened uncertainty skew risks sharply to the downside. In our view, a US recession will be a global recession. This time, Australia will not escape an economic downturn. The downside economic risk coincides with developed economy central banks with limited capacity to cut rates. These banks will need to turn to unconventional monetary policy to enhance their policy easing. In the US and in Australia, we expect that will take the form of quantitative easing (QE*). This outlook means the next 36 months will be a difficult time to navigate. Portfolios that are appropriately diversified, dynamically managed and aware of downside macro risk exposures will perform best.

Recession will take more than central banks can give

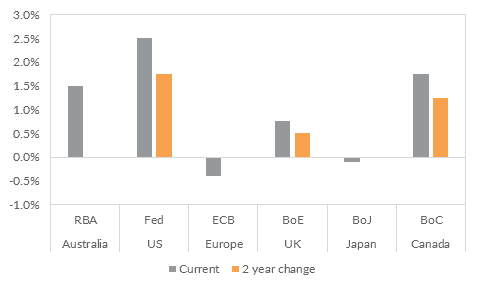

During a recession, the developed economy central banks have historically cut policy rates to engineer a recovery. We estimate that around 400-500bps of rate cuts are required to drive that recovery. Figure 1 shows the current policy settings of the major central banks. The US Fed is closest to having enough policy ammunition. The Fed Funds rate is currently at 2.50%. We expect it could increase to around 3.00%-3.25% over the next 18 months. In Australia, the RBA has a cash rate of 1.50%. We think that rate will remain unchanged through 2019 and be cut in 2020. Clearly, none of the banks could currently cut 400bps with going deeply into negative interest rate territory.

Figure 1: Central bank policy rates are low, and have been increased only gradually

Not all fixed income is defensive

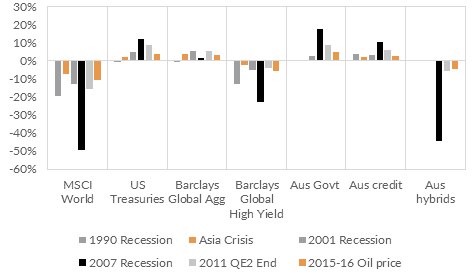

Recessions are not good times for risk assets. Figure 2 shows that unfortunately, recessions are also not good times for some assets often called “defensive”.

Figure 2: Asset performance during global market dislocations

Only the highest quality credits and fixed income really work as defensive assets during recessions and market dislocations. High yield and hybrids have not generally worked well. We think this will repeat in the next recession. Entering a downturn with low quality, high yielding credit in the portfolio runs the risk of mark-to-market losses and absolute loss of capital.

Only the highest quality credits and fixed income really work as defensive assets during recessions and market dislocations. High yield and hybrids have not generally worked well. We think this will repeat in the next recession. Entering a downturn with low quality, high yielding credit in the portfolio runs the risk of mark-to-market losses and absolute loss of capital.

Unconventional monetary policy: the new normal

The US Fed and Australian RBA will both implement QE to augment the available rate cuts, in our view. For the US Fed, this will likely be government purchases of US Treasuries or agency debt. The Fed has implemented this policy before during the period 2008 to 2013. The RBA is new to unconventional monetary policy but has the benefit of other central banks’ experience. Some key considerations will impact how the RBA implements QE.

- Fiscal strength: The Australian government is fiscally strong with low debt levels relative to the other developed economies. There is scope for some of the heavy lifting to be done by fiscal stimulus.

- Small debt markets: Australian bond markets are not large. A high portion is held by international investors. There is less scope for direct purchases of Australian government bonds to benefit the Australian economy compared against QE undertaken in the US.

- AUD support: The AUD will cushion the impact of a recession. We forecast the AUD to fall below USD0.65 during the recession. Over the next three years, we think sub-USD0.50 is more likely than USD0.80 or higher. A weaker AUD will provide some support to an economic recovery and reduce the amount of QE required.

- The housing market: In Australia, the monetary policy transmission mechanism is tied more closely to the cash rate. This compares to the US where the long-bond rate is crucial. Buying long-dated government bonds may not help drive mortgage rates lower to stimulate credit in Australia. And the housing market could also still be weak when the recession hits – reducing the impact of lower mortgage rates on credit demand.

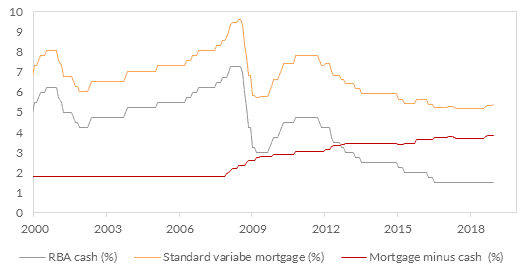

We think QE in Australia will be used to directly reduce the spread between the standard variable mortgage rate and the RBA cash rate. Figure 3 shows this spread has widened significantly post-GFC.

Figure 3: The spread between cash and mortgages has widened considerably

In Australia, QE will probably target this spread. Narrowing the spread back to 180bps – which persisted for 8.5 years through to December 2007 – would provide an extra 200+bps of easing to the Australian economy. That spread could be targeted by providing liquidity to banks via direct purchases of government-guaranteed banking debt.

In Australia, QE will probably target this spread. Narrowing the spread back to 180bps – which persisted for 8.5 years through to December 2007 – would provide an extra 200+bps of easing to the Australian economy. That spread could be targeted by providing liquidity to banks via direct purchases of government-guaranteed banking debt.

Now is the time to prepare

Our market and economic outlook over the next three years is challenging. Recessions can happen suddenly. The reaction in markets can be violent. We ultimately think central banks including the RBA will implement unconventional monetary policy to engineer stimulative monetary policy and a recovery in the real economy and asset markets. But now is the time to start preparing. Consulting a reliable portfolio advisor could be a start. Portfolios concentrated in risk assets are likely to suffer. We think that portfolios that are appropriately diversified will help. Markets will be volatile. We think that a clear, repeatable dynamic asset allocation process will help. Some assets will prove not to be defensive. We think that improving fixed income exposures will help. Please contact Oreana Financial Services or your affiliated Advisor to find out how we can assist with managing the risks to your portfolio.

*QE refers to unconventional monetary policies. It could include purchasing government bonds to keep long-term interest rates low. It could also include purchasing other financial assets to support liquidity and lending within an economy.

Data sources: Bloomberg LP, International Monetary Fund, Bank for International Settlements, Oreana Financial Services

This presentation material and all the information contained herein is the property of Oreana Financial Services Limited (OFS), and is protected from unauthorised copying and dissemination by copyright laws with all rights reserved. This presentation material, original or copy, is reserved for use by authorised personnel within OFS only and is strictly prohibited from public use and/or circulation. OFS disclaims any responsibility from any consequences arising from the unauthorised use and/or circulation of this presentation material by any party. This presentation material is intended to provide general information on the background and services OFS. No information within this presentation material constitutes a solicitation or an offer to purchase or sell any securities or investment advice of any kind. The analytical information within this presentation material is obtained from sources believed to be reliable. With respect to the information concerning investment referenced in this presentation material, certain assumptions may have been made by the sources quoted in compiling such information and changes in such assumptions may have a material impact on the information presented in this presentation material. In providing this presentation material, OFS makes no (i) express warranties concerning this presentation material; (ii) implied warranties concerning this presentation material (including, without limitation, warranties of merchantability, accuracy, or fitness for a particular purpose); (iii) express or implied warranty concerning the completeness or relevancy of this presentation material and the information contained herein. Past performance of the investment referenced in this presentation material is not necessarily indicative of future performance. Investment involves risks. Investors should refer to the Risk Disclosure Statements & Terms and Conditions of the relevant document for further details. This material has not been reviewed by the Securities and Futures Commission of Hong Kong.

Related Posts

Insights

Read our latest insights to help you make better investment decisions and build stronger portfolios.

Melbourne

Level 17, 627 Chapel Street, South Yarra, Melbourne, Victoria, 3141

Australia

T +61 3 9804 7113

F +61 3 9804 8377

Please email your request to

info@oreanafinancial.com

Sydney

Level 3, 31 Alfred Street,

Sydney, NSW 2000

Australia

T +61 3 9804 7113

F +61 3 9804 8377

Please email your request to

info@oreanafinancial.com

Hong Kong

Suite 1002, 10th Floor

Cambridge House, Taikoo Place

979 King’s Road, Quarry Bay, Hong Kong

T +852 3185 0200

F +852 2110 0736

Please email your request to

info@oreanafinancial.com

A Licensed Financial Firm

In Hong Kong we are licensed by the Securities and Futures Commission (license no. AHX191), the Insurance Authority (license no. FB1443) and the Mandatory Provident Fund Authority (license no. IC000563).

In Australia we are licensed by the Australian Securities and Investments Commission (AFSL No: 482234, ABN 91 607 515 122).