Search posts

First, the bad news

First, the bad news

In the US, jobs growth has slowed. Income growth is trending lower. Manufacturing peaked in 2018. Tense trade negotiations are taking place on multiple fronts. Inflationary pressures are low. Corporate credit has ballooned. But corporate credit quality has collapsed. US Treasury bond market are pricing rate cuts. Other developed market central banks have already cut rates. The global economy is edging closer to recession. That is the bad news. Global equity markets have seemingly taken this in their stride. A rally in the first week of June largely reversed the small sell-off in May. But that isn’t the good news. The good news is there is time to prepare. Right now, we think embracing dynamism and reviewing defensive exposures are the most pressing preparations for investors.

The US is edging towards recession

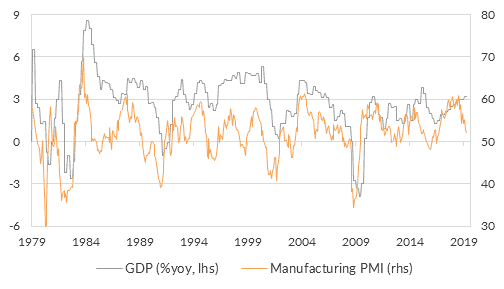

Economic growth probably peaked in 2018. GDP measured by expenditure suggests robust growth through Q1 2019. But GDP measured by income – theoretically equivalent – has trended lower. It is currently below 2%. Manufacturing surveys have also trended lower (Figure 1).

Figure 1: Manufacturing surveys suggest growth may have already peaked

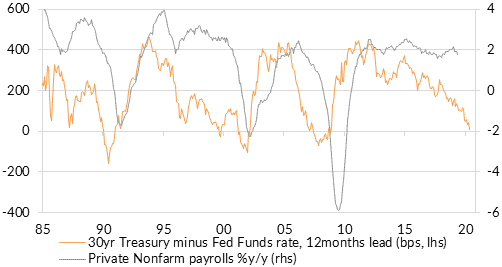

The May US payrolls report should also act as a wake-up call. The report was soft and recent jobs growth was revised lower. The yield curve, a leading indicator for jobs growth (Figure 2), suggests worse may be to come.

The May US payrolls report should also act as a wake-up call. The report was soft and recent jobs growth was revised lower. The yield curve, a leading indicator for jobs growth (Figure 2), suggests worse may be to come.

Figure 2: Volatility spiked suddenly in May following Presidential Tweets

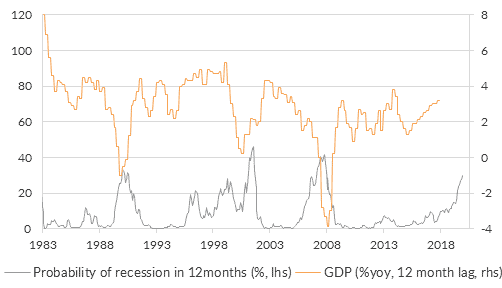

We think a recession could be driven by deteriorating credit quality in the US. Recently, the US investment grade index’s credit quality deteriorated to the point that BBB rated credit – the lowest investment grade – dominated the index. There could be other causes of recession. But whatever the cause, the odds of a recession in the next year are increasing (Figure 3). And if there is a US recession, it will be a global recession.

We think a recession could be driven by deteriorating credit quality in the US. Recently, the US investment grade index’s credit quality deteriorated to the point that BBB rated credit – the lowest investment grade – dominated the index. There could be other causes of recession. But whatever the cause, the odds of a recession in the next year are increasing (Figure 3). And if there is a US recession, it will be a global recession.

Figure 3: The NY Fed model of recession probability is higher than in July 2007

Bond markets are pricing cuts, but not enough

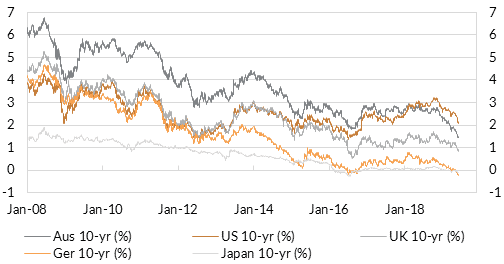

World bond markets agree with the gloomy outlook (Figure 4). In the US, three rate cuts are priced with better than 50% probability by end-2019. In Australia, the RBA has already cut. We expect QE will be required in both markets.

Figure 4: Government bond yields have declined as the outlook as deteriorated

Equity markets have rallied in early June as yields declined. Equity investors may be expecting global central banks to engineer a soft landing for the slowing economy. But soft landings are rare. Typically, as rate cuts are priced in and implemented, the yield curve steepens. This coincides with a decrease in corporate profits and increases in equity and credit risk premia. The combination tends to drive a violent re-rating lower in equity and credit prices.

Equity markets have rallied in early June as yields declined. Equity investors may be expecting global central banks to engineer a soft landing for the slowing economy. But soft landings are rare. Typically, as rate cuts are priced in and implemented, the yield curve steepens. This coincides with a decrease in corporate profits and increases in equity and credit risk premia. The combination tends to drive a violent re-rating lower in equity and credit prices.

What actions can be taken?

The good news is, investors can prepare for these downside risks. Now is the time to implement appropriate, repeatable, fundamentals based dynamic asset allocation. Having a clear sense of potential risk-adjusted returns over the medium-term is important. This process removes the temptation to try and time market movements. Now is also the time to build exposure to real defensive assets. That means moving up the capital structure and focusing on the highest grade credit available. Developed market sovereign bonds still offer good risk-adjusted returns, despite low starting yields. High yield credit, lower quality loans and hybrids are likely to suffer equity like drawdowns and capital losses. We cannot stress enough that we expect these instruments are unlikely to provide defensiveness to investment portfolios.

Conclusion

First, the bad news. The risks to the economy are skewed to the downside. Many asset valuations are stretched. Potential returns are skewed to the downside as a result. The good news is, there is still time to prepare. The recent economic trends are a call to action to implement appropriate, repeatable dynamic asset allocation processes. Reviewing defensive asset exposure is an important part of that process. Failing to act could result in considerable drawdowns or loss of capital. Contact Oreana Financial Services or your affiliated Advisor to find out how we can assist with managing your wealth.

Data sources: Bloomberg LP, Oreana Financial Services

This presentation material and all the information contained herein is the property of Oreana Financial Services Limited (OFS), and is protected from unauthorised copying and dissemination by copyright laws with all rights reserved. This presentation material, original or copy, is reserved for use by authorised personnel within OFS only and is strictly prohibited from public use and/or circulation. OFS disclaims any responsibility from any consequences arising from the unauthorised use and/or circulation of this presentation material by any party. This presentation material is intended to provide general information on the background and services OFS. No information within this presentation material constitutes a solicitation or an offer to purchase or sell any securities or investment advice of any kind. The analytical information within this presentation material is obtained from sources believed to be reliable. With respect to the information concerning investment referenced in this presentation material, certain assumptions may have been made by the sources quoted in compiling such information and changes in such assumptions may have a material impact on the information presented in this presentation material. In providing this presentation material, OFS makes no (i) express warranties concerning this presentation material; (ii) implied warranties concerning this presentation material (including, without limitation, warranties of merchantability, accuracy, or fitness for a particular purpose); (iii) express or implied warranty concerning the completeness or relevancy of this presentation material and the information contained herein. Past performance of the investment referenced in this presentation material is not necessarily indicative of future performance. Investment involves risks. Investors should refer to the Risk Disclosure Statements & Terms and Conditions of the relevant document for further details. This material has not been reviewed by the Securities and Futures Commission of Hong Kong.

Related Posts

Insights

Read our latest insights to help you make better investment decisions and build stronger portfolios.

Melbourne

Level 17, 627 Chapel Street, South Yarra, Melbourne, Victoria, 3141

Australia

T +61 3 9804 7113

F +61 3 9804 8377

Please email your request to

info@oreanafinancial.com

Sydney

Level 3, 31 Alfred Street,

Sydney, NSW 2000

Australia

T +61 3 9804 7113

F +61 3 9804 8377

Please email your request to

info@oreanafinancial.com

Hong Kong

Suite 1002, 10th Floor

Cambridge House, Taikoo Place

979 King’s Road, Quarry Bay, Hong Kong

T +852 3185 0200

F +852 2110 0736

Please email your request to

info@oreanafinancial.com

A Licensed Financial Firm

In Hong Kong we are licensed by the Securities and Futures Commission (license no. AHX191), the Insurance Authority (license no. FB1443) and the Mandatory Provident Fund Authority (license no. IC000563).

In Australia we are licensed by the Australian Securities and Investments Commission (AFSL No: 482234, ABN 91 607 515 122).