Search posts

Australian Tax Residency Proposed Changes

The 2021-22 Australian Federal Budget included an announcement that set out to simplify the individual tax residency rules for Australians. A proposal that initially seemed a positive announcement may hold a number of consequences for current Australian expats as well as those looking to move overseas for employment in the future. We take a look at how these proposed changes will work and some possible scenarios.

How will the proposed changes work?

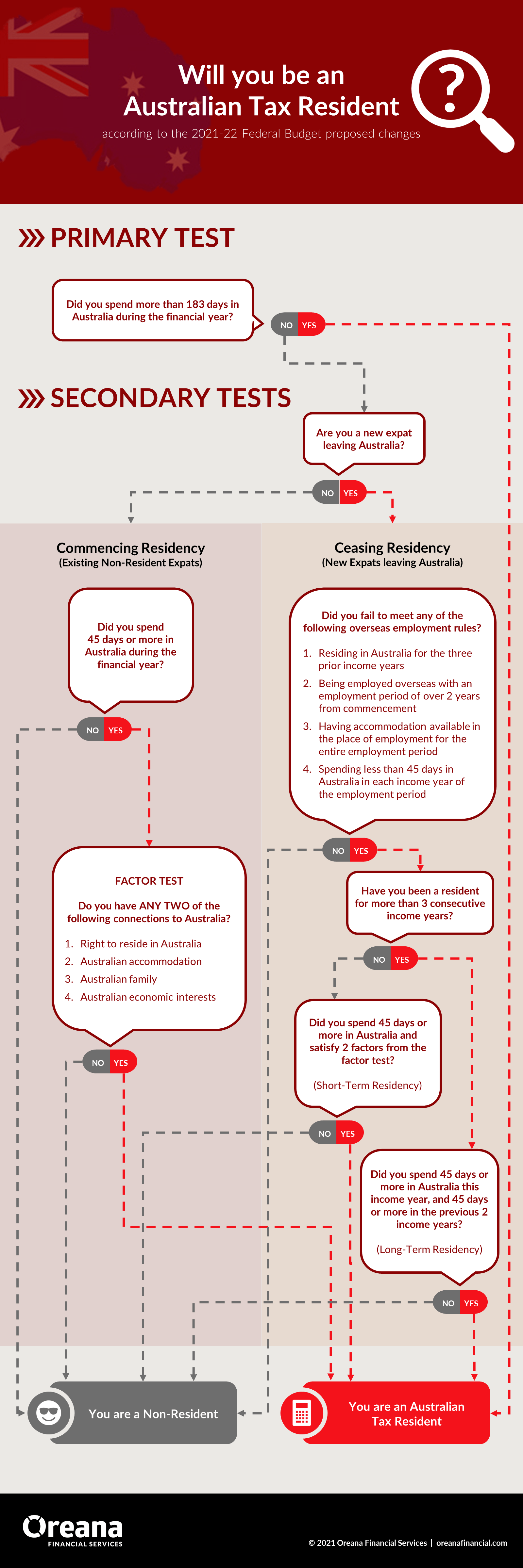

The changes which are detailed in a report from the Board of Taxation completed in 2019, will be based on a primary test as well as secondary tests. The Primary Test is clear and states if you spend more than 183 days in Australia you will be an Australian tax resident. If you have not been in Australia for more than 183 days, you will need to meet the secondary tests. The Secondary Tests include a test for commencing residency which would include existing expats who are currently non-tax residents, as well as ceasing residency which would include those leaving Australia for employment overseas looking to become non-tax residents.

COMMENCING RESIDENCY

45 Day Test – Did you spend 45 days in Australia?

- No – you are a non-tax resident

- Yes – apply the factor test

The Factor Test – The factor test states where you have spent more than 45 days in Australia, and if you meet any 2 of the following tests you will be deemed as an Australian Tax Resident:

- Right to reside permanently in Australia – This includes Citizens and Permanent residents, which means most Australian expats will meet this factor.

- Australian accommodation – You have a property available for your use when in Australia. This could include an empty property or the use of

- Australian family – Spouse, and/or any children under the age of 18 that live in Australia on an ongoing basis during an income year.

- Australian economic interests – employment in Australia or actively participating in carrying on a business. Australian assets such as taxable Australian property, significant cash in bank accounts, or an interest in a family trust.

CEASING RESIDENCY

Employment Test – If you satisfy the below employment rules, you will be a non-resident from the day you leave Australia:

- Residing in Australia for the three prior income years.

- Being employed overseas with an employment period of over 2 years from commencement.

- Having accommodation available in the place of employment for the entire employment period.

- Spending less than 45 days in Australia in each income year of the employment period.

If you do not satisfy the above rules you will need to determine if you are a short or long term resident. You will be a short-term resident if you have been an Australian tax resident for less than three years, and a long term resident if more than 3 years.

- Short Term Resident – Have you spent less than 45 days in Australia and meet less than 2 factors from the factor test?

- Yes – You are a non-tax resident from the day you leave Australia

- No – You will remain an Australian Tax Resident

- Long Term Resident – Did you spend less than 45 days in Australia this income year, and less than 45 days in the previous 2 income years?

- Yes – You are a non-tax resident

- No – You will remain an Australian Tax Resident

Here is a flowchart to help you understand more easily:

Double Tax Agreement (DTA)

Australia has a double tax agreement with a number of countries, which will essentially provide a tie-breaker test when you are determined to be a tax resident of both Australia and the country that you reside in. Unfortunately for expats in Hong Kong, it does not have a DTA with Australia, while countries such as Singapore and Thailand do have a DTA with Australia. The test is based on 3 key factors:

- Having a permanent home in one country and not the other, or

- Having a habitual abode in one country and not the other, or

- Having personal and economic relations strongest in one country and not the other

Under the DTA for an expat residing in Singapore, if you meet one of these factors such as having your permanent home in Singapore and not in Australia, you would likely meet the test and deemed be a tax resident of Singapore only.

Possible Scenarios

If I am an expat, and my spouse and children live in Australia, will I be caught under these new rules? If you spend 45 days or more in Australia visiting your family, you will then trigger the factor test. Based on being a citizen or PR of Australia and having your spouse and children residing in Australia, you would meet two tests and be deemed an Australian resident for tax purposes. What are the implications if I do become an Australian tax resident? How much tax will I have to pay? Based on an example income of $200,000 you would pay tax of only $21,150 in Singapore, and $64,667 in Australia. This highlights the substantial difference in tax and the importance of ensuring you are aware of how the proposed changes may impact you. If I spend 7 days in Australia in August on holidays and then decide to repatriate to Australia in March the following year, when will I be deemed to commence Australian tax residency? Under the 45 day and factor test, your tax residency will commence from the 1st day you are physically present in Australia. This would mean your residency would likely commence when you arrived in August.

In Summary

While the proposal does provide expats with greater certainty around tax residency, many current expats may unintentionally be caught out under the proposed rules which could have large unintended financial consequences. It is important to note that the proposed changes are not yet law and will only come into effect from 1 July of the year after the proposal has been made law. While this means there is the possibility it will come into effect from 1 July 2021, it is more likely that it will be 1 July 2022 or 1 July 2023. If you are unsure of how the proposed changes affect your personal situation, it is important to plan for the change now. Please contact us to discuss your personal situation.

This presentation material and all the information contained herein is the property of Oreana Financial Services Limited (OFS), and is protected from unauthorised copying and dissemination by copyright laws with all rights reserved. This presentation material, original or copy, is reserved for use by authorised personnel within OFS only and is strictly prohibited from public use and/or circulation. OFS disclaims any responsibility from any consequences arising from the unauthorised use and/or circulation of this presentation material by any party. This presentation material is intended to provide general information on the background and services OFS. No information within this presentation material constitutes a solicitation or an offer to purchase or sell any securities or investment advice of any kind. The analytical information within this presentation material is obtained from sources believed to be reliable. With respect to the information concerning investment referenced in this presentation material, certain assumptions may have been made by the sources quoted in compiling such information and changes in such assumptions may have a material impact on the information presented in this presentation material. In providing this presentation material, OFS makes no (i) express warranties concerning this presentation material; (ii) implied warranties concerning this presentation material (including, without limitation, warranties of merchantability, accuracy, or fitness for a particular purpose); (iii) express or implied warranty concerning the completeness or relevancy of this presentation material and the information contained herein. Past performance of the investment referenced in this presentation material is not necessarily indicative of future performance. Investment involves risks. Investors should refer to the Risk Disclosure Statements & Terms and Conditions of the relevant document for further details. This material has not been reviewed by the Securities and Futures Commission of Hong Kong.

Related Posts

Insights

Read our latest insights to help you make better investment decisions and build stronger portfolios.

Melbourne

Level 17, 627 Chapel Street, South Yarra, Melbourne, Victoria, 3141

Australia

T +61 3 9804 7113

F +61 3 9804 8377

Please email your request to

info@oreanafinancial.com

Sydney

Level 3, 31 Alfred Street,

Sydney, NSW 2000

Australia

T +61 3 9804 7113

F +61 3 9804 8377

Please email your request to

info@oreanafinancial.com

Hong Kong

Suite 1002, 10th Floor

Cambridge House, Taikoo Place

979 King’s Road, Quarry Bay, Hong Kong

T +852 3185 0200

F +852 2110 0736

Please email your request to

info@oreanafinancial.com

A Licensed Financial Firm

In Hong Kong we are licensed by the Securities and Futures Commission (license no. AHX191), the Insurance Authority (license no. FB1443) and the Mandatory Provident Fund Authority (license no. IC000563).

In Australia we are licensed by the Australian Securities and Investments Commission (AFSL No: 482234, ABN 91 607 515 122).