Search posts

Listen to the Fed

At the November FOMC policy meeting, the US Federal Reserve announced it would slow the pace of its asset purchases. This is a process known as tapering. The Fed well and truly forewarned markets it was coming. The clear communication prevented a bond market sell-off, or “taper tantrum”. The Fed also indicated that rate hikes were some way off. We agree.

“Transitory” is over

The direction for policy rates is higher. Inflation is well above the Fed’s target. It won’t fall below in a hurry.

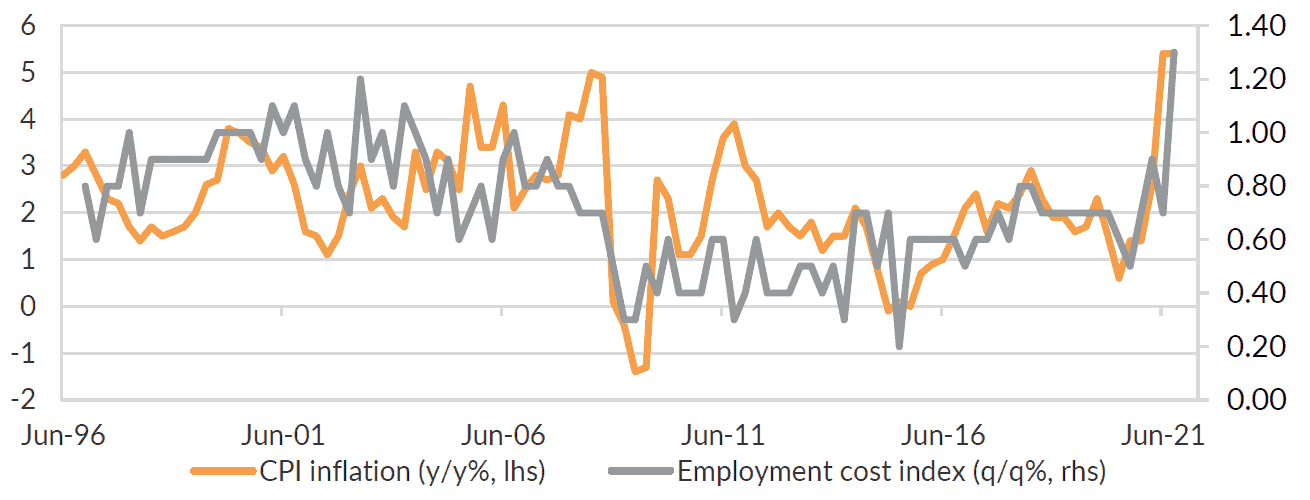

Figure 1: Employment costs and inflation have spiked higher in the US

The US employment cost index increased by the most in 31 years, in Q3. Productivity growth and labour supply will ease this somewhat. But we expect inflation will be at or a bit above the Fed’s target for the medium-term.

Rate hikes are some way off

Markets have moved to price rate hikes by next year. The Fed’s dot plot – the estimates for future rates from Fed members – agrees. Both have been terrible indicators for the timing of rate hikes over the past decade. The Fed is right to say rate hikes are some way off. We think that will be late 2022 at the earliest, but more likely 2023.

Yields are moving higher

Higher inflation and uncertainty around the timing for rates means term premium will widen. That will push nominal bond yields higher.

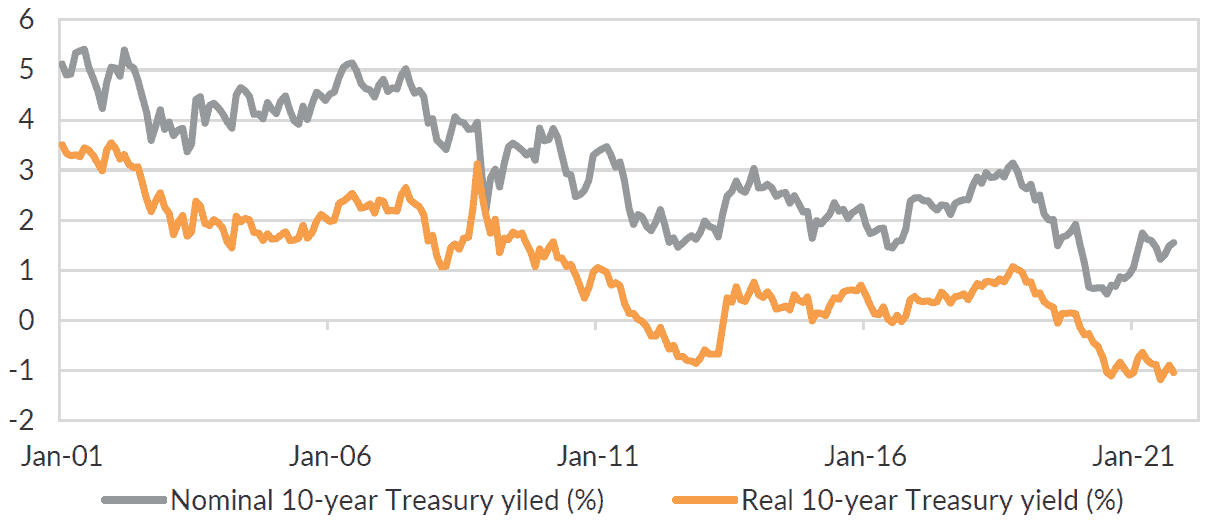

We focus on the real (inflation adjusted) yield. The US 10-year real Treasury yield is deeply negative. That indicates investors are still willing to hold a negative yielding asset, rather than invest into productive capacity in the real economy. We anticipate that real yield will move higher over 2022 as the global economy re-reopens. That will be a positive sign for the economic outlook.

Figure 2: The real yield is too low and needs to move higher before policy rates lift off

Higher bond yields, higher inflation, solid growth, solid earnings

US equities have climbed to fresh record highs following the Fed’s tapering announcement. But higher yields come with some risk for equities. Higher yields will be challenging to digest if they are not matched by solid growth and solid earnings.

We expect solid economic growth over 2022 and 2023. This will be partly driven by a re-reopening of the US economy. We also expect an increase in capital expenditure as companies choose to invest in productive capacity rather than hold low (negative) yielding assets.

Solid economic growth should support earnings in the near- to medium-term. That will continue to support equity returns, despite a move higher in yields.

It won’t be all one-way traffic

The path higher for equities and yields will be punctuated by periods of volatility. Markets will over extrapolate rate hikes. They will over-react to negative economic data flow. Global risks including Chinese property, oil prices, political challenges and global conflict will impact the pathway. But we still think we are early in the economic and asset price cycle. That means investors should look through near-term noise and remain invested.

Contact PAS for more information

The Portfolio Advisory Service has been working with clients across Australia and Asia to help manage investment solutions. Our work is supported by deep asset class research and manager review expertise within the team.

Reach out to our Portfolio Advisory Service to find out how we can assist you with managing your investment challenges.

This presentation material and all the information contained herein is the property of Oreana Financial Services Limited (OFS), and is protected from unauthorised copying and dissemination by copyright laws with all rights reserved. This presentation material, original or copy, is reserved for use by authorised personnel within OFS only and is strictly prohibited from public use and/or circulation. OFS disclaims any responsibility from any consequences arising from the unauthorised use and/or circulation of this presentation material by any party. This presentation material is intended to provide general information on the background and services OFS. No information within this presentation material constitutes a solicitation or an offer to purchase or sell any securities or investment advice of any kind. The analytical information within this presentation material is obtained from sources believed to be reliable. With respect to the information concerning investment referenced in this presentation material, certain assumptions may have been made by the sources quoted in compiling such information and changes in such assumptions may have a material impact on the information presented in this presentation material. In providing this presentation material, OFS makes no (i) express warranties concerning this presentation material; (ii) implied warranties concerning this presentation material (including, without limitation, warranties of merchantability, accuracy, or fitness for a particular purpose); (iii) express or implied warranty concerning the completeness or relevancy of this presentation material and the information contained herein. Past performance of the investment referenced in this presentation material is not necessarily indicative of future performance. Investment involves risks. Investors should refer to the Risk Disclosure Statements & Terms and Conditions of the relevant document for further details. This material has not been reviewed by the Securities and Futures Commission of Hong Kong.

Related Posts

Insights

Read our latest insights to help you make better investment decisions and build stronger portfolios.

Melbourne

Level 17, 627 Chapel Street, South Yarra, Melbourne, Victoria, 3141

Australia

T +61 3 9804 7113

F +61 3 9804 8377

Please email your request to

info@oreanafinancial.com

Sydney

Level 3, 31 Alfred Street,

Sydney, NSW 2000

Australia

T +61 3 9804 7113

F +61 3 9804 8377

Please email your request to

info@oreanafinancial.com

Hong Kong

Suite 1002, 10th Floor

Cambridge House, Taikoo Place

979 King’s Road, Quarry Bay, Hong Kong

T +852 3185 0200

F +852 2110 0736

Please email your request to

info@oreanafinancial.com

A Licensed Financial Firm

In Hong Kong we are licensed by the Securities and Futures Commission (license no. AHX191), the Insurance Authority (license no. FB1443) and the Mandatory Provident Fund Authority (license no. IC000563).

In Australia we are licensed by the Australian Securities and Investments Commission (AFSL No: 482234, ABN 91 607 515 122).