Search posts

Portfolio masterclass: diversification

Diversification is one of the most fundamental yet misunderstood concepts in investment management. When diversification is applied well, it is a critical portfolio management tool. However, when used without appropriate due process, it can lead to significant drawdowns in times where it should have insulated the portfolio from significant shocks.

What is diversification?

There is well-known investment adage: Don’t put all your eggs in one basket. Simply stated, the term “diversification” is used to describe the allocation of capital (the eggs) across multiple assets (the baskets).

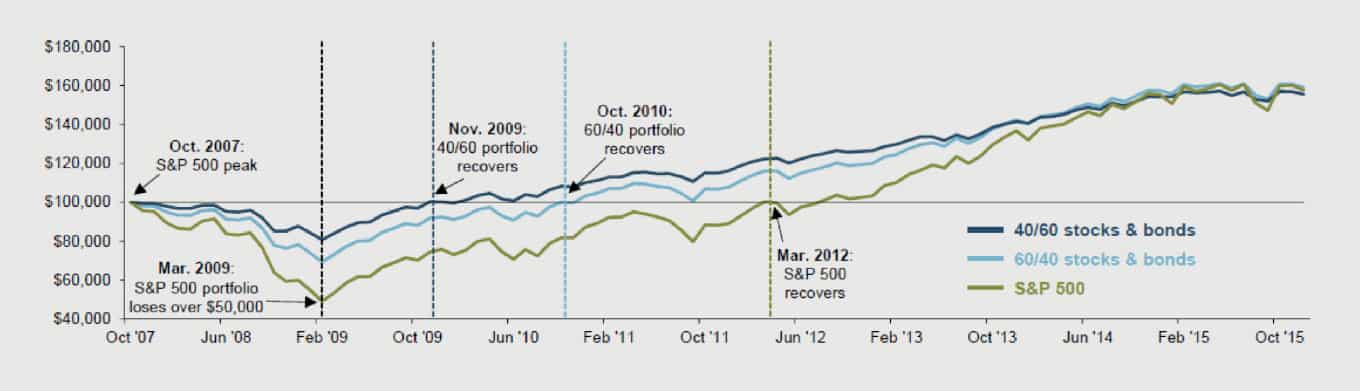

To demonstrate: Let us take the S&P 500 Index as a proxy for equities; and the Barclays U.S. Aggregate Index as the proxy for bonds (Fig. 1), we can see the effects of diversification. Expressed as “moderate” and “balanced” portfolios, capital is respectively allocated across growth (equities) and defensive assets (bonds) in a 40/60 and 60/40 split.

Fig. 1: Portfolio returns: Stocks vs stock and bond blend; Source: J.P. Morgan.

Most poignant here is that by blending stocks and bonds together in an investment portfolio, it also reduces the overall variability (or risk) of a given portfolio – one of the key benefits of diversification. This means that the portfolio returns over time is essentially “smoothed” by combining the two asset classes together – resulting in a more comfortable ride.

Even by using a relatively naïve form of diversification such as the one demonstrated in Fig. 1, we can easily see the impact of combining multiple assets together. If we were to take a more sophisticated approach, we will start to look for assets that have a tendency to behave differently – something financial pundits like to call assets that express “low correlation” to each other.

Correlation

The key to efficient diversification involves the statistical concept of correlation. Correlation measures the degree to which two assets move together. The perfect positive correlation is 1.0, or 100%. For example, two assets that always move up and down in together (though possibly by different amounts), they will exhibit correlation of close to 1.0. If we were to combine these two assets together, no diversification is achieved.

At the other end, the perfect negative correlation is -1.0, or -100%. In this case, two assets will always move in the opposite direction. Assets that exhibit perfect negative correlation again do not work well in an investment portfolio – if one asset increases by $1 and the other one falls by $1, then we are left with $0 (loss or gain) but the exposure has taken up time and the investor has to wear transaction costs – not an ideal investment outcome.

In actual fact, the assets we actually want to add to an investor’s portfolio are assets which exhibit low correlation to traditional markets. As a general rule, assets which exhibit a correlation of between -0.2 to 0.2 reflects little to no relationship to each other. Use of these assets with low correlation to traditional markets can provide significant benefits for investment outcomes for investors.

Assets with Low Correlation to Traditional Markets – “alternative” assets

Identifying these assets can be tricky. Assets that exhibit low correlation to traditional assets during “normal” market conditions may, in times of financial stress or heightened market volatility, exhibit a marked spike in correlations – exactly what the purposes of diversification is supposed to insulate against. When everyone rushes for the exits, people are going to get hurt, and the same can be said for financial assets when a selling frenzy takes hold.

However, there are a broad range of strategies and assets which are not as sensitive to the price movements in the listed markets or more crowded trades. These include market neutral hedge funds, some infrastructure, real property, and some private debt tranches like mezzanine finance.

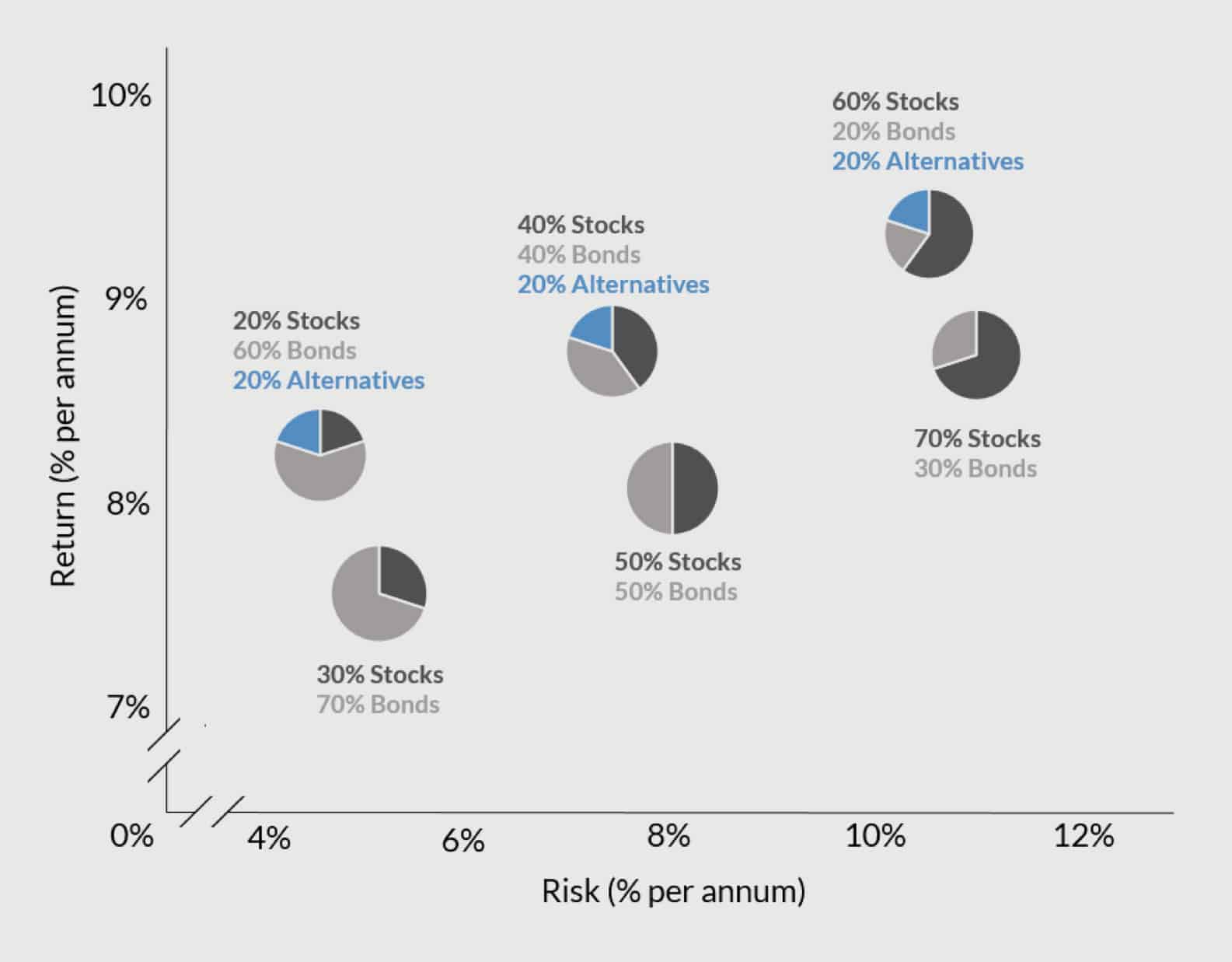

The introduction of some of these alternative assets to the stocks/bonds mix is depicted in Fig. 2 below. Using historical returns, it is possible to generate a picture of what is possible through the appropriate use of alternatives. In certain allocations, it has been shown to achieve a higher return with the same amount of risk, or the same amount of return with a lower risk.

Fig.2: Using Alternatives in a traditional portfolio; Source: Oreana; Factset; Note: the chart is a simplified blend of ex-post returns from 1990 to 2015. Stocks is represented by S&P 500 Index; bonds represented by Barclays U.S. Aggregate Index; alternatives represented by a blend of 10% in hedge funds and 10% in real property.

In order to identify the appropriate strategies and assets to use, it is important to use caution. For example, some of these strategies can be complex or rely on certain market conditions. Finally, managers of these assets need to have the right skill-set, have appropriate systems, processes and procedures and the right business environment.

At Oreana Asset Management, we use our internal and external expertise within the Asia region and beyond to bring both traditional and non-traditional assets to investors. Please contact us or your financial advisor if you wish to discuss your investment needs.

Related Posts

Insights

Read our latest insights to help you make better investment decisions and build stronger portfolios.

Melbourne

Level 17, 627 Chapel Street, South Yarra, Melbourne, Victoria, 3141

Australia

T +61 3 9804 7113

F +61 3 9804 8377

Please email your request to

info@oreanafinancial.com

Sydney

Level 3, 31 Alfred Street,

Sydney, NSW 2000

Australia

T +61 3 9804 7113

F +61 3 9804 8377

Please email your request to

info@oreanafinancial.com

Hong Kong

Suite 1002, 10th Floor

Cambridge House, Taikoo Place

979 King’s Road, Quarry Bay, Hong Kong

T +852 3185 0200

F +852 2110 0736

Please email your request to

info@oreanafinancial.com

A Licensed Financial Firm

In Hong Kong we are licensed by the Securities and Futures Commission (license no. AHX191), the Insurance Authority (license no. FB1443) and the Mandatory Provident Fund Authority (license no. IC000563).

In Australia we are licensed by the Australian Securities and Investments Commission (AFSL No: 482234, ABN 91 607 515 122).