Search posts

When markets yield to fundamentals

In June last year we wrote that our base case view was for a US – and global – recession by end-2020. In January our 2019 Medium-Term Global Outlook warned that now was the time to prepare for recession, to prevent panic later. In March 2019 we warned that recession made QE likely in both the US and Australia. We spoke about the inverted yield curve in December 2018. And over the past 5 months we have observed global and Australian economic data grind towards levels consistent with the start of a recession. Market volatility is on the rise and the sugar rush from central bank rate cuts will not last. Stretched asset prices are giving way to a weak set of economic fundamentals. Historically that has resulted in significant wealth destruction. There is still time to prepare portfolios for that recessionary outcome. But time is running out. We urge that it is time to act now.

The fundamentals have not improved

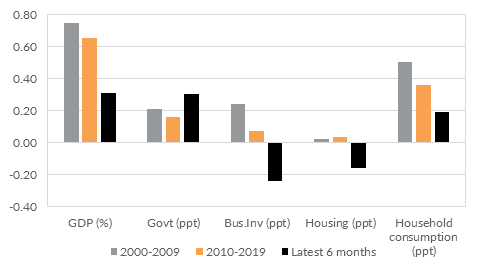

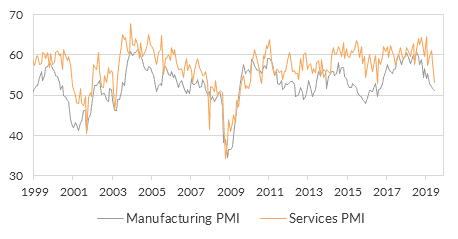

We have watched the US and global economy slide towards recession over the past year. Already most of the developed global economy is in or about to enter a manufacturing or industrial recession. That includes the US and Australia (Fig 1 and Fig 2).

Fig 1: Australian business investment has been a drag on GDP for the past 6 months

Fig 2: US PMIs are sliding into recession levels

Central banks will need to do more

There is a tension between cheap liquidity from central banks and deteriorating economic fundamentals. We discussed this in August 2019. Central banks around the world will be forced to do more to prevent a deeper, longer recession. That includes the RBA in Australia. We expect QE will ultimately be required. We discussed what that might look for like Australia in March 2019.

Volatility will increase

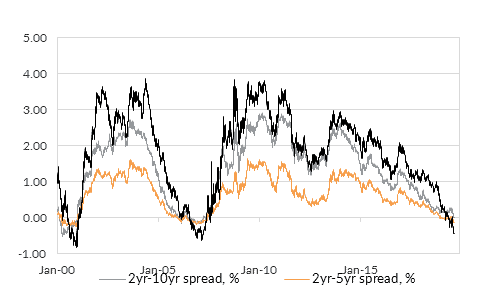

We expect increasing market volatility as the tension plays out. More recently, the inversion in the yield curve (Fig 3) – where longer-dated US Treasury yields are lower than shorter-dated – has focused attention on recessionary outcomes. The curve has inverted before every recession since the 1950s. We talked about this back in December 2018. The recent inversion supports our thesis that we are headed for a period of higher volatility.

Fig 3: The US Treasury yield curve has inverted

What does it mean for Australian investors?

We expect Australia will not escape a global recession. Australia’s private sector demand is very weak (Fig 1). And we don’t think households, nor the housing sector, will ride to the rescue. We set out some recommendations for Australian investors early in 2019 in our Oreana Medium-Term Global Outlook. We warned that now is the time to prepare, not panic. The specific recommendations for Australian investors remain relevant. The recommendations were: – Now is the time to review exposure to Australian equities: Australian equities have historically cumulatively fallen around 30% during US recessions. We see downside risks particularly to equities exposed to the housing cycle. – Now is the time to reduce credit exposure: Australian corporate credit is generally investment grade. But it has not passed the test of being truly defensive. We prefer defensive exposure in investment grade sovereign debt. – Now is the time to consider reducing your AUD hedge ratio: We expect the AUD will weaken in the near term. During recessionary periods, the AUD has historically moved in a risk-off manner, falling to levels much lower than currently priced in the forward market. – Now is the time to increase exposure to alternatives: Alternatives are assets that are not just exposed to long positions in equity or debt. Alternatives provide important diversifying benefits. We think alternatives should be a significant element of any portfolio.

Now is the time to prepare

Time is running out to implement these recommendations. Implementing well requires time, expertise and scale. But the benefit to portfolios could be truly transformative over the medium-term for investor outcomes. We urge investors to consider making some of these changes. Contact Oreana Financial Services or your affiliated Advisor to find out how we can assist with managing your wealth.

Data sources: Bloomberg LP, Oreana Financial Services

This presentation material and all the information contained herein is the property of Oreana Financial Services Limited (OFS), and is protected from unauthorised copying and dissemination by copyright laws with all rights reserved. This presentation material, original or copy, is reserved for use by authorised personnel within OFS only and is strictly prohibited from public use and/or circulation. OFS disclaims any responsibility from any consequences arising from the unauthorised use and/or circulation of this presentation material by any party. This presentation material is intended to provide general information on the background and services OFS. No information within this presentation material constitutes a solicitation or an offer to purchase or sell any securities or investment advice of any kind. The analytical information within this presentation material is obtained from sources believed to be reliable. With respect to the information concerning investment referenced in this presentation material, certain assumptions may have been made by the sources quoted in compiling such information and changes in such assumptions may have a material impact on the information presented in this presentation material. In providing this presentation material, OFS makes no (i) express warranties concerning this presentation material; (ii) implied warranties concerning this presentation material (including, without limitation, warranties of merchantability, accuracy, or fitness for a particular purpose); (iii) express or implied warranty concerning the completeness or relevancy of this presentation material and the information contained herein. Past performance of the investment referenced in this presentation material is not necessarily indicative of future performance. Investment involves risks. Investors should refer to the Risk Disclosure Statements & Terms and Conditions of the relevant document for further details. This material has not been reviewed by the Securities and Futures Commission of Hong Kong.

Related Posts

Insights

Read our latest insights to help you make better investment decisions and build stronger portfolios.

Melbourne

Level 17, 627 Chapel Street, South Yarra, Melbourne, Victoria, 3141

Australia

T +61 3 9804 7113

F +61 3 9804 8377

Please email your request to

info@oreanafinancial.com

Sydney

Level 3, 31 Alfred Street,

Sydney, NSW 2000

Australia

T +61 3 9804 7113

F +61 3 9804 8377

Please email your request to

info@oreanafinancial.com

Hong Kong

Suite 1002, 10th Floor

Cambridge House, Taikoo Place

979 King’s Road, Quarry Bay, Hong Kong

T +852 3185 0200

F +852 2110 0736

Please email your request to

info@oreanafinancial.com

A Licensed Financial Firm

In Hong Kong we are licensed by the Securities and Futures Commission (license no. AHX191), the Insurance Authority (license no. FB1443) and the Mandatory Provident Fund Authority (license no. IC000563).

In Australia we are licensed by the Australian Securities and Investments Commission (AFSL No: 482234, ABN 91 607 515 122).